Managing New Wealth Wisely: Planning for Private School Fees After a Windfall

Introduction

Coming into a large sum of money can be life-changing. Whether through inheritance, the sale of a business, a divorce settlement, or another significant event, sudden wealth can bring both opportunity and responsibility.

For many, one of the first goals after receiving new wealth is to create a sense of security for their family. Providing children or grandchildren with a high-quality private education often sits at the top of that list.

Private education continues to grow in popularity for its smaller class sizes, individualised attention, and broader extracurricular opportunities. The Independent Schools Council (ISC) reports that 556,551 pupils now attend 1,411 member schools, the highest number since records began in 1974.¹

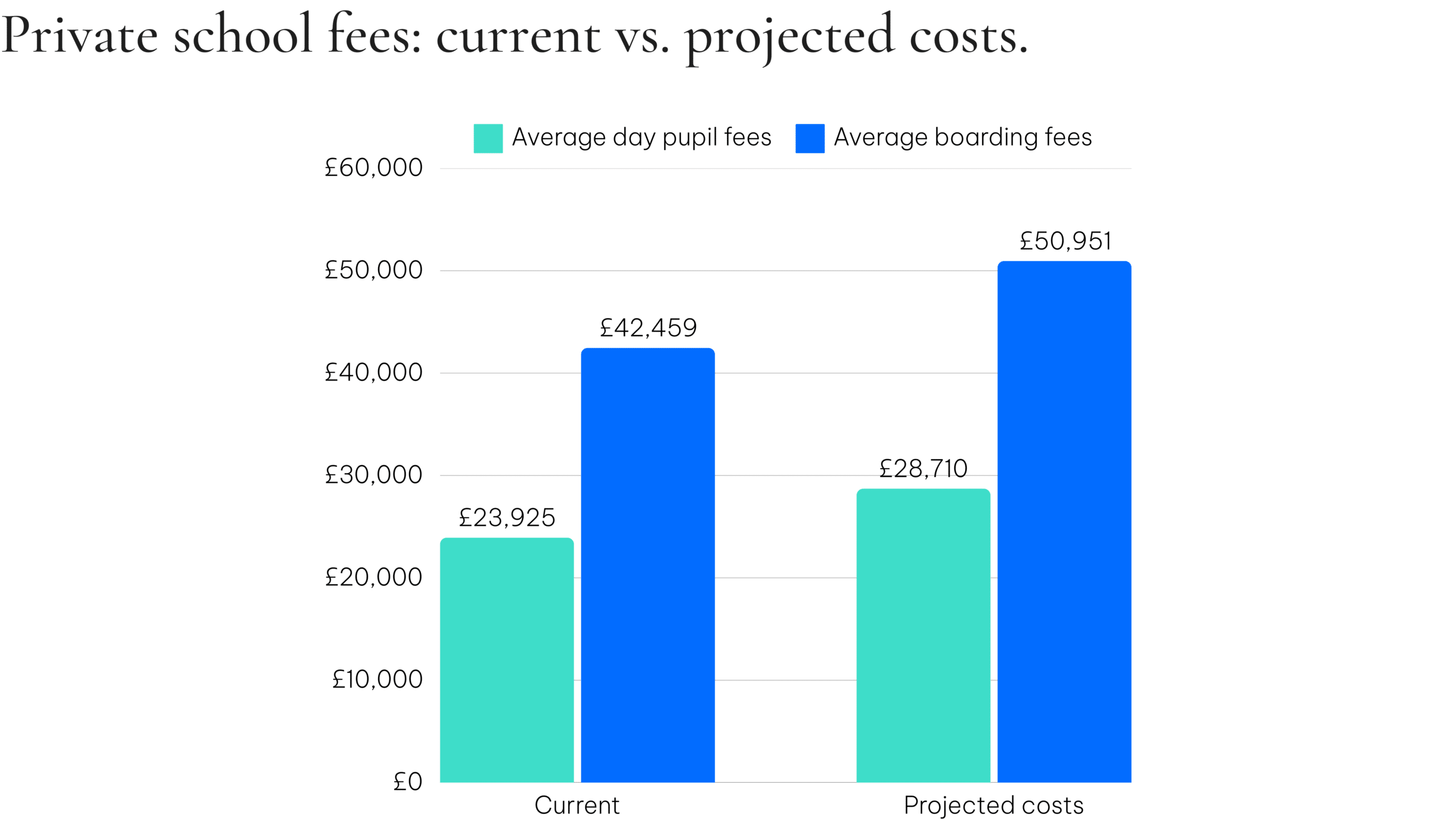

However, the cost of this investment is substantial. The average day pupil fee is now £23,925 per year, rising to £42,459 for boarding students.² With VAT on school fees to be introduced in January 2025, those figures could rise to £28,710 and £50,951 respectively.

Across a full education, that equates to around £460,000 in day pupil fees or £815,000 in boarding fees per child. For anyone managing newly acquired wealth, planning how to allocate funds toward these costs while preserving capital for the long term is essential.

1, 2 ISC Census and Annual Report, January 2024

At a glance

- School fees may reach £460,000–£815,000 per child.

- Early planning helps manage cash flow and preserve capital.

- ISAs, Bonds, and GIAs offer flexible, tax-efficient investment options.

- Building structure into new wealth creates long-term stability.

Take Your Autumn Statement Impact Assessment

Start NowMaking Thoughtful Financial Decisions

Receiving a sudden influx of money can be emotionally overwhelming. It often comes during a significant life event, such as the passing of a loved one, the sale of a long-held asset, or a major personal transition. It can be tempting to make quick financial decisions, but taking time to plan strategically can make a lasting difference.

Private school fees represent a meaningful, long-term commitment. Approaching them as part of a comprehensive wealth plan ensures that your new assets work for both immediate goals and your family’s financial future.

Building a Long-Term Plan After a Windfall

Let’s assume school fees increase by 3.5% per year, one of the lowest growth rates in recent years. Even so, the total cost of education remains significant. Establishing a structured, tax-efficient plan can help you meet these expenses comfortably while protecting your capital from unnecessary tax exposure.

Many recipients of sudden wealth find value in separating funds into distinct categories: immediate needs, medium-term goals, and long-term investments. Setting aside a portion of your new wealth for education within a well-diversified investment strategy helps balance access to funds with growth potential.

Key tax-efficient solutions

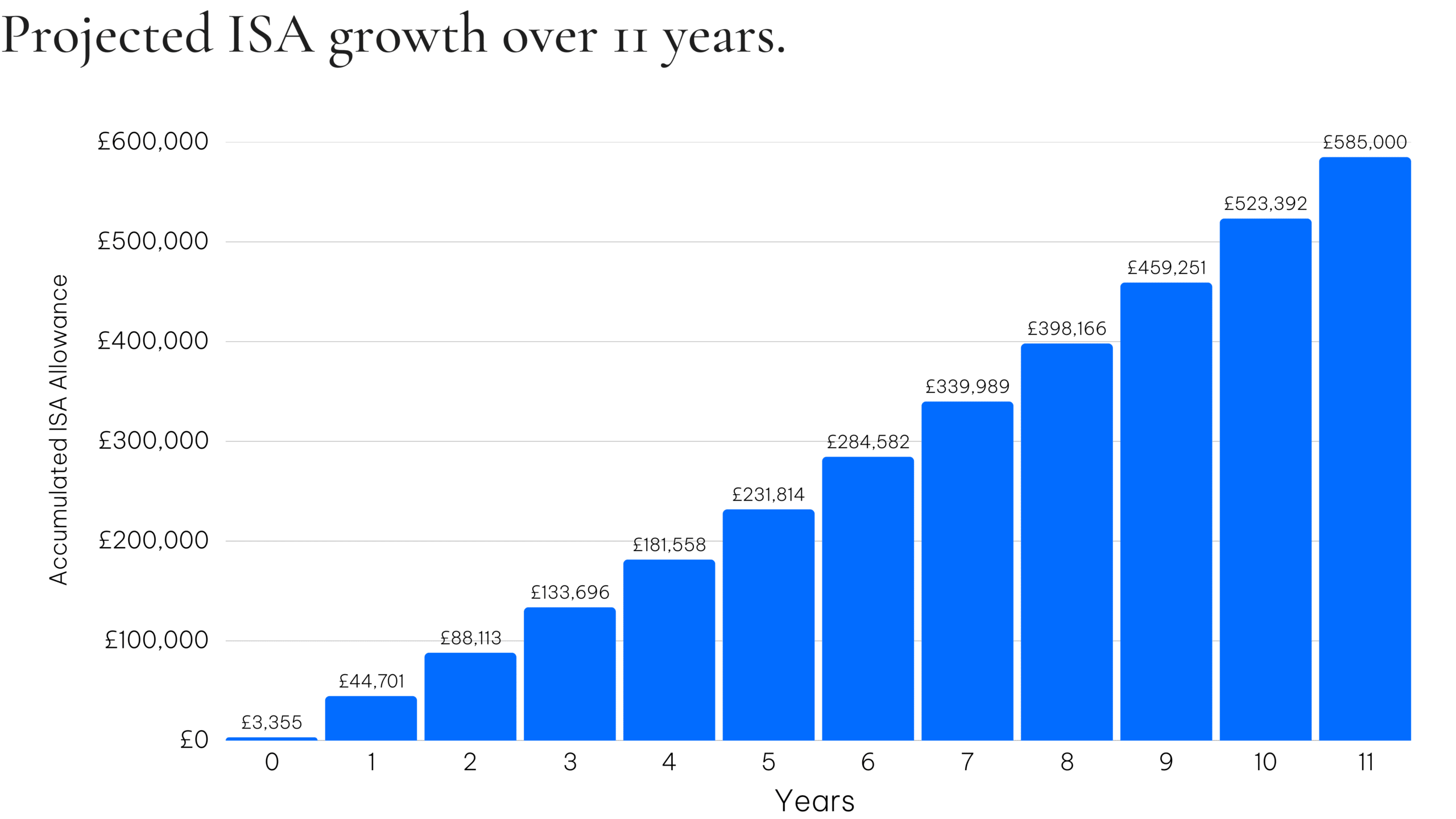

ISAs are one of the simplest and most tax-efficient ways to save or invest part of your new wealth. You can contribute up to £20,000 per adult per tax year (2024/25), and all growth and withdrawals are free from income and capital gains tax.

For someone managing new wealth, ISAs provide both flexibility and peace of mind. If both parents contribute the full allowance from a child’s birth and achieve 5% net annual growth, this could grow to around £585,000 by the time the child turns 11 (illustrative only).

ISAs allow you to access funds when needed, which makes them ideal for covering school fees in stages while keeping the remainder invested for growth.

*These figures are examples only and they are not guaranteed – they are not minimum or maximum amounts. What you get back depends on how your investment grows and the tax treatment of the investment.

The value of an ISA with St. James’s Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested.

The favourable tax treatment of ISAs may be subject to changes in legislation in the future.

Investment Bonds are another useful structure for managing newly acquired wealth. They allow you to invest a lump sum or make regular contributions while deferring tax on growth.

During the life of the bond, returns are not immediately subject to income or capital gains tax, allowing the investment to compound more efficiently. You can withdraw up to 5% of your original investment each year for up to 20 years without triggering an immediate tax charge. Any unused allowance can roll forward.

This structure provides flexibility and control, helping you draw income gradually to pay for education while keeping the remainder invested. Offshore bonds may also offer additional tax planning benefits, depending on your personal situation.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

Please note that if the withdrawals taken exceed the growth of the bond, the capital will be eroded.

If you have already used your ISA allowance, Unit Trusts and General Investment Accounts (GIAs) can provide a flexible way to invest across a range of assets, including shares, bonds, and property funds.

They currently benefit from a £500 dividend allowance and a £3,000 capital gains allowance (2024/25). While these allowances are limited, they can be managed strategically to optimise your tax position.

For those managing new wealth, these accounts can help keep funds accessible while still targeting long-term growth. This can be useful when you want to retain liquidity for major expenses such as school fees or future property purchases.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

If you wish to support education costs for children or grandchildren, the £3,000 annual gifting allowance (£6,000 for couples) provides a simple and tax-efficient way to do so.

Larger gifts can also be exempt from inheritance tax (IHT) if the donor survives seven years, or if payments are made from regular surplus income. For new wealth recipients, using gifting allowances effectively can be an important part of long-term estate planning.

Parents can also pay for education directly under the “Dispositions for the maintenance of children” rules, which means those payments are not considered transfers for IHT purposes.

A disposition is exempt if it is:

– made in favour of a child of either party to a marriage or civil partnership, and

– for that child’s maintenance or education before the age of 18, or while in full-time education.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

Further criteria applies within the HMRC IHT Manual IHTM04175 which is subject to change.

Many private schools offer financial support to families through bursaries or scholarships. About one-third of pupils in private education receive some level of assistance.³

Bursaries are awarded based on family means, while scholarships recognise academic or extracurricular excellence. Even partial awards can help extend how far your new wealth goes.

3 ISC School Fee Assistance, April 2023

If you have received a significant lump sum, some schools offer discounts for paying fees in advance. This can lock in costs and reduce future outgoings.

However, before making a large prepayment, weigh the benefits against the potential returns that could be achieved by keeping the funds invested. Liquidity and flexibility are often valuable when managing a new financial situation.

A diversified investment plan may offer greater long-term benefit than an upfront discount, depending on your goals and risk tolerance.

Preserving Wealth After a Windfall

Sudden wealth can provide lifelong security, but only if it is managed carefully. Structuring your finances to balance income, growth, and protection helps preserve value over time.

Diversifying across different investment vehicles and using tax wrappers effectively can prevent unnecessary erosion of capital. You may also wish to explore trusts or estate planning solutions to safeguard assets for future generations.

Working with an experienced adviser can help you navigate the emotional and financial decisions that come with new wealth, ensuring that generosity toward family sits within a clear, sustainable plan.

Creating a Lasting Legacy

Education support is one of the most enduring ways to create a legacy. It allows you to invest in your family’s potential while seeing the impact of your wealth in your lifetime.

By planning carefully, you can use your new financial position to fund education, build stability, and leave a foundation for future generations. Thoughtful planning ensures that your sudden wealth translates into lasting wellbeing and opportunity for those you care about most.

Conclusion

Sudden wealth brings both freedom and responsibility. While private education is a valuable and meaningful way to use new financial resources, it should be approached as part of a comprehensive plan that also preserves your long-term financial security.

By combining tax-efficient investing, structured withdrawals, and thoughtful estate planning, you can support your family’s education goals and safeguard your wealth for years to come.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time and depend on individual circumstances.

Should you require more information or have particular questions, we invite you to contact us at your convenience.

Contact Us

Nauman Gondal

Chief Executive Officer