Rebuilding Financial Confidence: Planning for Private School Fees After Divorce

Introduction

Divorce or separation brings major changes, not only emotionally but financially too. Rebuilding your financial life can take time and careful planning. For many separated parents, ensuring that children continue to receive the education they deserve is a top priority, even as household income and budgets adjust.

Private education remains highly sought after for its smaller class sizes, individual attention, and broad curriculum. The Independent Schools Council (ISC) reports that 556,551 pupils now attend 1,411 member schools, the highest number since records began in 1974.¹

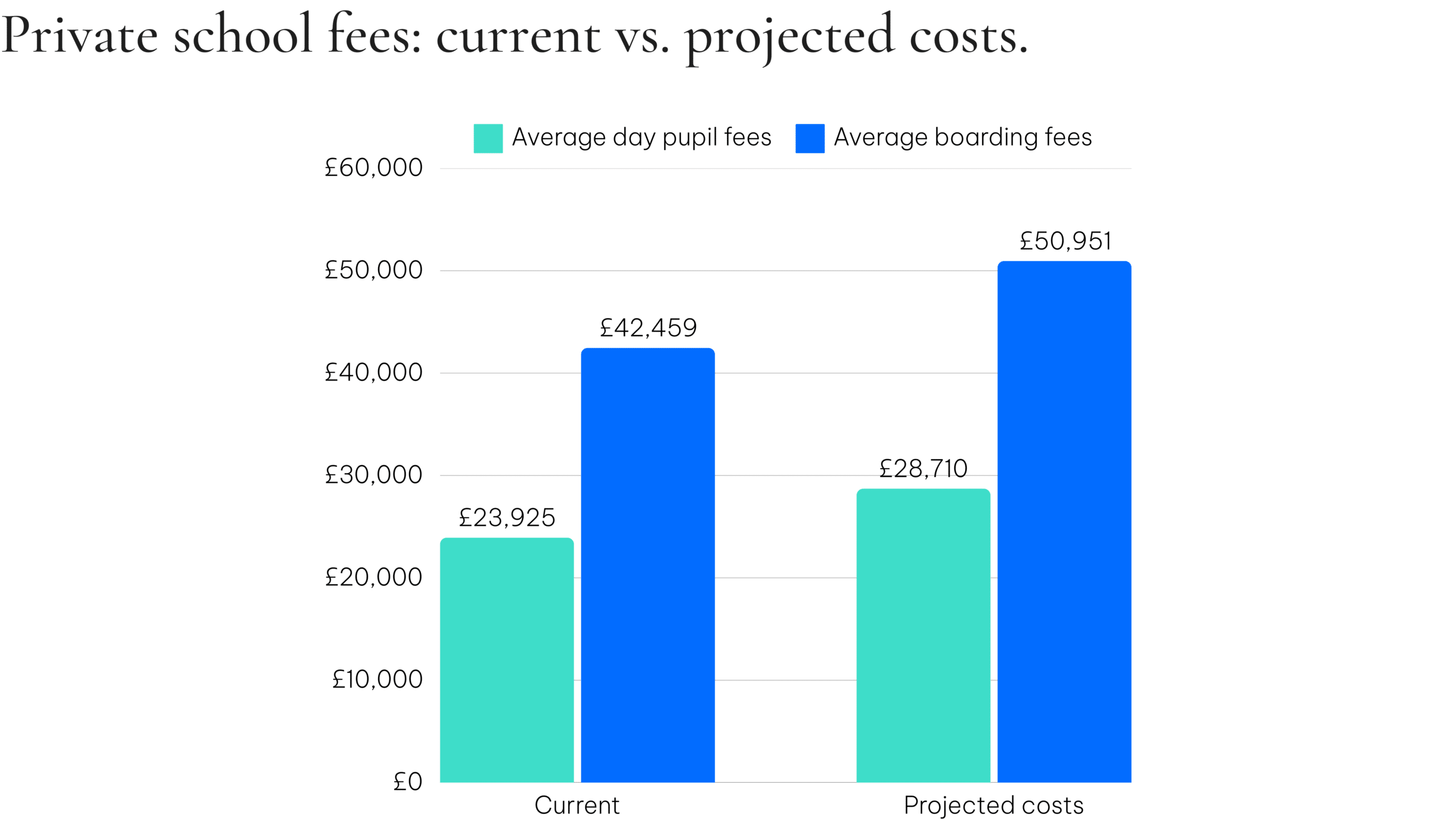

However, the cost of providing this level of education is significant. The average day pupil fee is now £23,925 per year, rising to £42,459 for boarding pupils.² With VAT on school fees due from January 2025, the average day fee is expected to rise to £28,710, and boarding fees to £50,951.

Over a full school career, that means parents could face total costs of around £460,000 for day schooling or £815,000 for boarding per child. For separated families managing two households, planning ahead is essential to maintain stability and keep educational goals on track.

1, 2 ISC Census and Annual Report, January 2024

At a glance

- School fees may reach £460,000–£815,000 per child.

- Early planning helps manage shared responsibilities and cash flow.

- ISAs, Bonds, and GIAs offer flexible, tax-efficient investment options.

- Agreements about contributions and funding sources protect everyone’s interests.

Take Your Autumn Statement Impact Assessment

Start NowBalancing Education Costs After Divorce

After separation, many parents find that their financial responsibilities change dramatically. Income may now come from one household instead of two, and new expenses such as housing or legal fees can make budgeting more complex.

Despite these changes, many parents remain committed to maintaining continuity in their children’s education. That is why it is so important to approach school fees as part of a wider financial plan that supports both short-term needs and long-term security.

Open communication and planning can help you and your former partner find fair and workable solutions for sharing costs, whether through direct contributions, trust arrangements, or structured withdrawals from savings and investments.

Planning for Stability and Control

Let’s assume school fees increase by 3.5% per year, a relatively conservative estimate. Even at that rate, the cumulative cost is substantial.

Having a clear, written plan for how school fees will be funded provides confidence for everyone involved. You may wish to review cash flow, investment portfolios, or maintenance agreements to determine the most tax-efficient and sustainable approach.

If you have received a financial settlement or lump sum, allocating part of those funds toward an education investment strategy can help ensure school fees are met without disrupting your future financial independence.

Key tax-efficient solutions

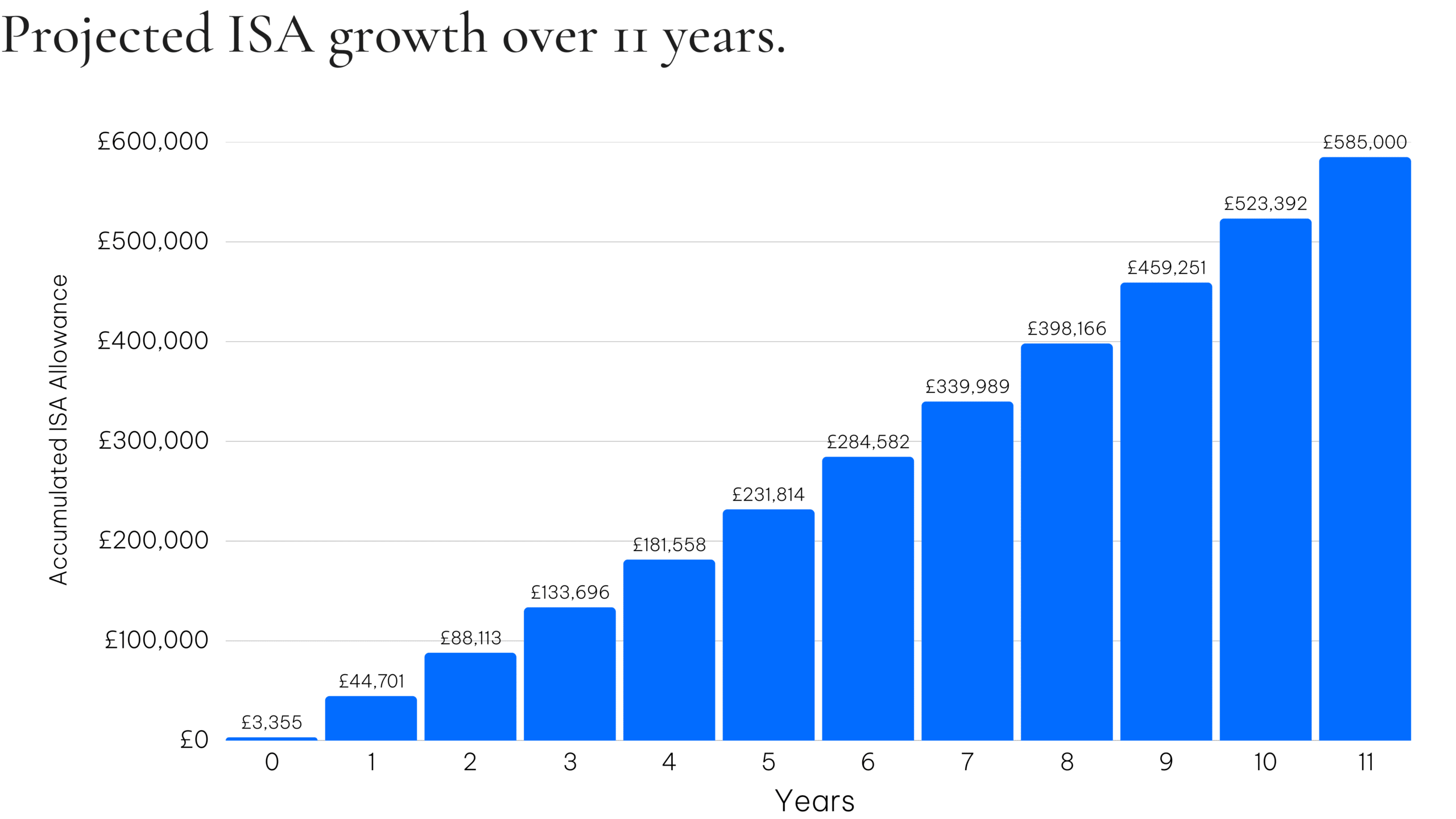

ISAs are one of the most accessible ways to save and invest for school fees. You can invest up to £20,000 per adult per tax year (2024/25), and all income and growth within the ISA are free from income and capital gains tax.

If both parents contribute regularly and achieve 5% net annual growth, this could amount to £585,000 by the time the child is 11 years old (illustrative only).

For separated parents, ISAs offer flexibility and control. Funds can be accessed at any time, and each parent can maintain independent ownership of their savings while working toward a shared goal.

*These figures are examples only and they are not guaranteed – they are not minimum or maximum amounts. What you get back depends on how your investment grows and the tax treatment of the investment.

The value of an ISA with St. James’s Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested.

The favourable tax treatment of ISAs may be subject to changes in legislation in the future.

Investment Bonds can provide a structured way to manage larger sums from a divorce settlement or asset division. These allow you to invest either a lump sum or regular contributions while deferring tax on growth.

You can withdraw up to 5% of your original investment each year for up to 20 years without triggering an immediate income or capital gains tax charge. This structure can be useful for covering school fees over time, while the remaining capital continues to grow.

For separated parents, bonds can also help with long-term planning and inheritance arrangements, ensuring funds are preserved for children’s education in a controlled, tax-efficient way.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

Please note that if the withdrawals taken exceed the growth of the bond, the capital will be eroded.

For additional flexibility, Unit Trusts and GIAs offer a straightforward way to invest in a range of assets, including shares, bonds, and property.

They benefit from a £500 dividend allowance and a £3,000 capital gains allowance (2024/25). While gains and income may be taxable, these investments provide easy access to funds and can be managed to suit your income needs and tax position.

For example, a GIA might hold investments earmarked for school fees, allowing withdrawals as needed, while other assets are reserved for your own retirement or home purchase plans.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

If grandparents or extended family wish to help, the £3,000 annual gifting allowance (£6,000 for couples) provides a tax-efficient way to contribute toward education costs.

Larger gifts can also be exempt from inheritance tax (IHT) if the donor survives seven years, or if payments are made from regular surplus income. Parents can also make direct payments for education under the “Dispositions for the maintenance of children” rules, meaning these are not considered transfers for IHT purposes.

A disposition is exempt if it is:

– made in favour of a child of either party to a marriage or civil partnership, and

– for that child’s maintenance or education before the age of 18, or while in full-time education.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

Further criteria applies within the HMRC IHT Manual IHTM04175 which is subject to change.

Private schools often offer bursaries and scholarships, which can make education more affordable. About one-third of pupils in private education receive some form of support.³

Bursaries are awarded based on financial need, while scholarships recognise achievement in areas such as academics, music, or sport. These can help reduce the financial burden on separated families and allow children to remain in their existing schools where possible.

3 ISC School Fee Assistance, April 2023

If your divorce settlement included a lump sum, you may have the option to prepay school fees. Many schools offer discounts for advance payments, which can simplify budgeting and reduce long-term costs.

However, consider whether retaining the funds and investing them instead could produce higher returns over the same period. Maintaining access to capital can be important as you adjust to a new financial situation and set future goals.

After divorce, ensuring that you and your children remain financially secure is key. Reviewing life insurance, income protection, wills, and guardianship arrangements helps safeguard your family’s future.

It is also important to revisit pension and investment strategies to reflect your new financial independence. A clear, updated plan provides confidence that education costs and other long-term goals remain achievable.

Should you require more information or have particular questions, we invite you to contact us at your convenience.

Contact Us

Nauman Gondal

Chief Executive Officer