Invest Early, Grow Smart: Funding Private Education the Tax-Efficient Way

Introduction

You’re earning well, your career is accelerating, and your future looks promising. Like many High Earners, Not Rich Yet (HENRYs), you may have a strong income but limited accumulated assets after rent, mortgages, or student loans.

As you start planning long-term goals such as home ownership or starting a family, private education for future children may be one of them. Independent schools continue to attract more families, with 556,551 pupils now enrolled in 1,411 ISC schools, the highest since records began in 1974.¹

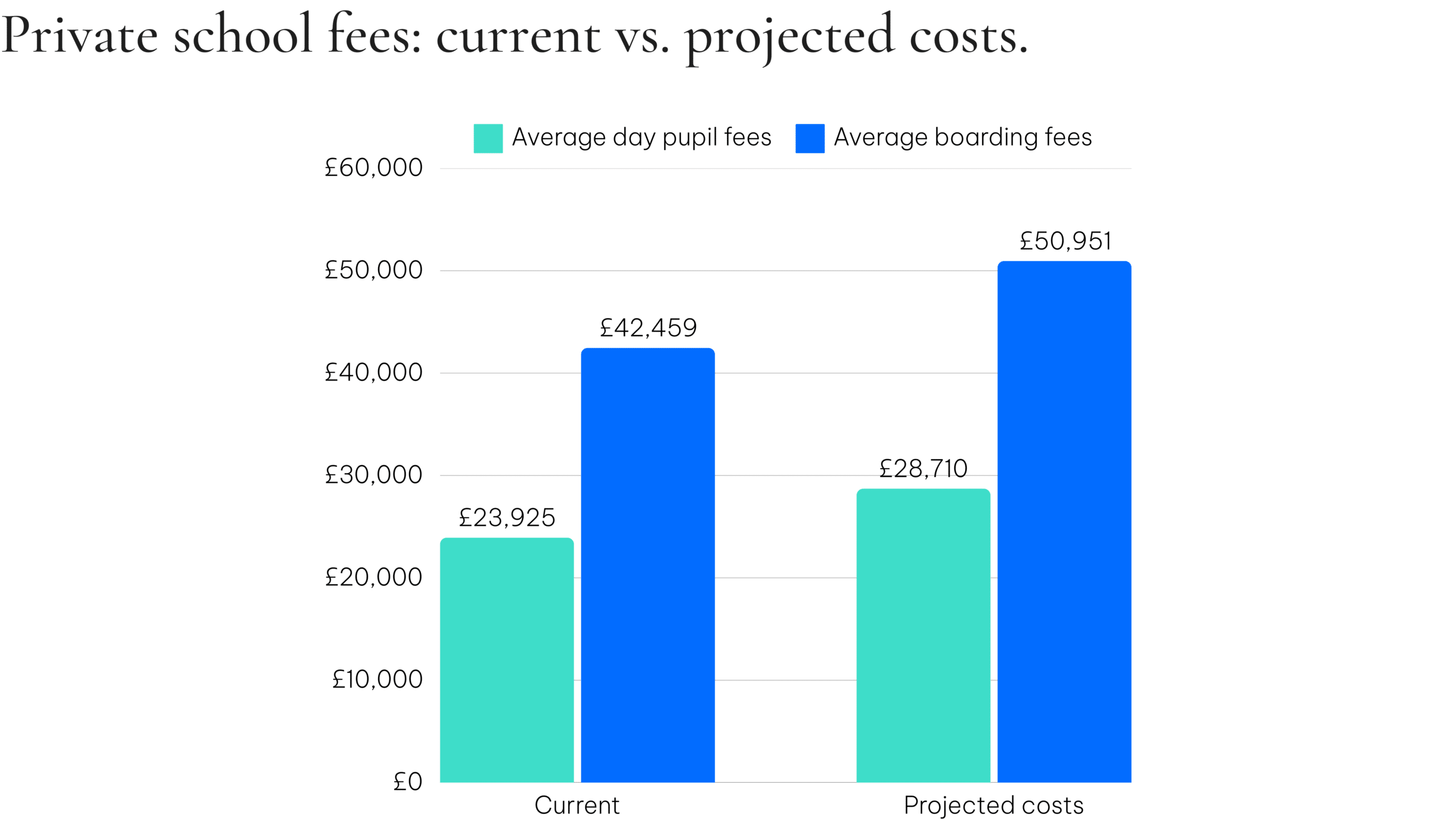

However, opportunity comes with cost. The average annual day fee is now £23,925, rising to £42,459 for boarders.² With VAT on school fees from January 2025, these could reach £28,710 and £50,951 respectively. That represents around £460,000–£815,000 per child over their full education.

For high-earning professionals, the key is simple: start early, invest consistently, and let compounding work in your favour.

1, 2 ISC Census and Annual Report, January 2024

At a glance

- Average school fees could exceed £460,000 per child.

- Starting early allows compounding to do the heavy lifting.

- ISAs, Bonds, and GIAs can grow funds tax-efficiently.

- Consistent investing builds discipline and long-term wealth.

Take Your Autumn Statement Impact Assessment

Start NowStart Early, Benefit More

School fees typically rise around 3.5% per year, and compounding applies to costs as well as investments. Waiting until you need the funds means playing catch-up, while starting now allows your savings to grow with you.

Even modest monthly contributions invested regularly can build substantial capital over a decade or more. Investing early provides freedom and flexibility later, whether for school fees, property, or other life goals.

Planning While You Build Wealth

Early-career professionals face a common challenge: strong income but competing financial priorities. Balancing lifestyle spending, debt repayment, and investing takes discipline, but every pound you invest today can multiply through compound growth.

The right investment vehicles help you grow wealth steadily while keeping future goals tax-efficient and accessible.

Key tax-efficient solutions

ISAs are a simple and flexible way to start investing. Each adult can contribute up to £20,000 per year (2024/25), with all income and capital growth sheltered from tax.

By investing monthly from early adulthood, you can build a strong base for future education costs even before starting a family.

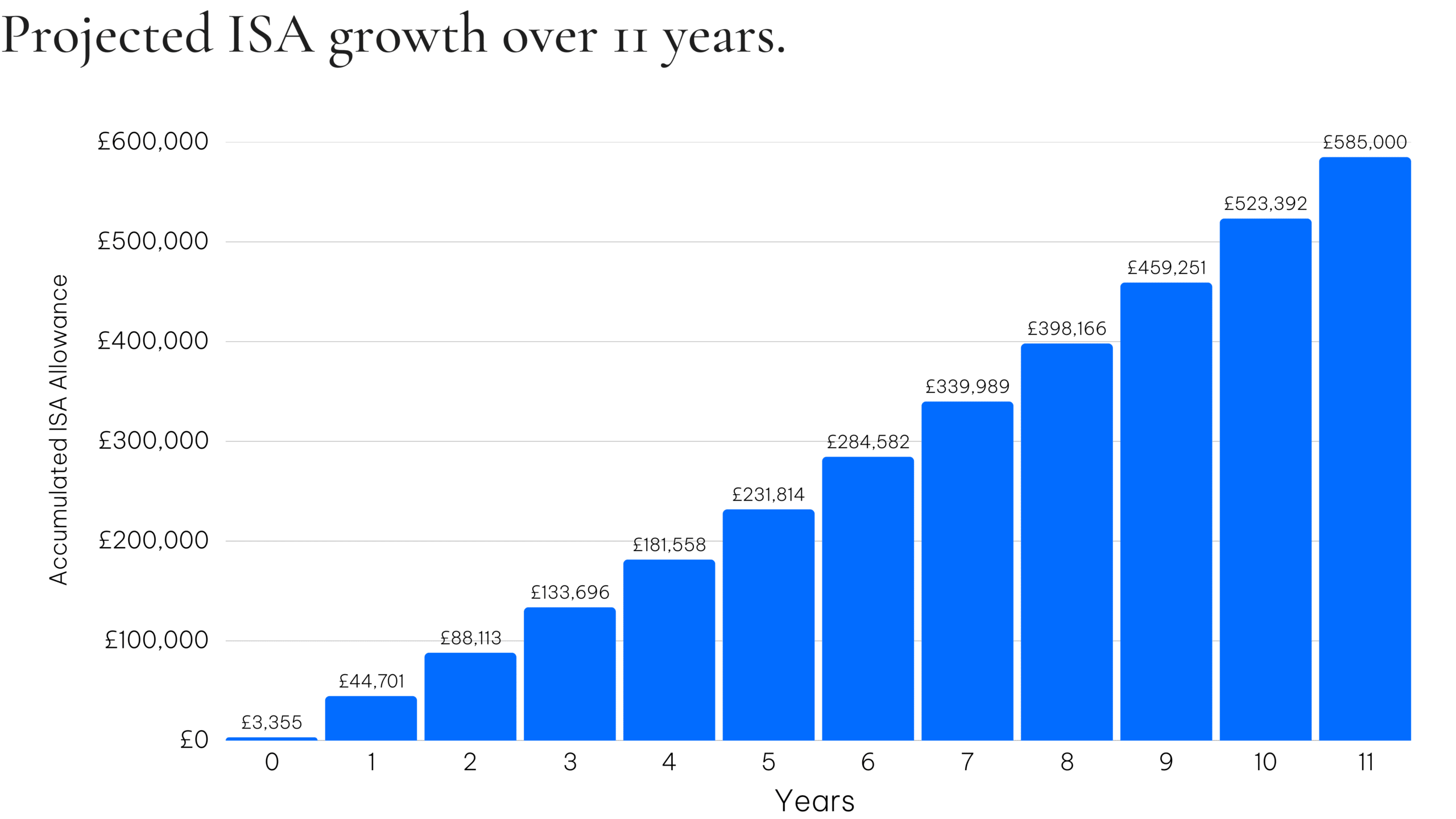

If both partners invest their full allowances annually from a child’s birth and achieve 5% net growth, savings could total around £585,000 by age 11 (illustrative only). Withdrawals are tax-free and unrestricted, giving full control when you need funds.

*These figures are examples only and they are not guaranteed – they are not minimum or maximum amounts. What you get back depends on how your investment grows and the tax treatment of the investment.

The value of an ISA with St. James’s Place will be directly linked to the performance of the funds selected and may fall as well as rise. You may get back less than you invested.

The favourable tax treatment of ISAs may be subject to changes in legislation in the future.

Investment Bonds allow you to grow capital tax-deferred, which is useful if your earnings and tax rate are likely to rise over time. You can withdraw up to 5% of the original investment per year for 20 years without immediate income or capital gains tax.

Unused withdrawal allowances can roll forward, allowing flexible drawdown in the years school fees begin. Bonds can also be suitable for bonuses or equity awards that you wish to invest for the long term in a tax-efficient way.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

Please note that if the withdrawals taken exceed the growth of the bond, the capital will be eroded.

Once you have used your ISA allowance, GIAs and Unit Trusts provide flexibility and access to a wide range of investments. They can hold equities, bonds, and other assets to help you build long-term wealth.

These accounts benefit from a £500 dividend allowance and a £3,000 capital-gains allowance (2024/25). While taxable, they are useful for those who value liquidity and control over when gains are realised.

The value of an investment with St. James’s Place will be directly linked to the performance of the funds you select and the value can therefore go down as well as up. You may get back less than you invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

If family support is available, for example from parents or grandparents, the £3,000 annual gifting allowance (£6,000 per couple) provides a tax-efficient way to build education funds on your behalf.

Larger gifts can also qualify for inheritance-tax (IHT) exemption if the donor survives seven years or if payments are made from surplus income. For those starting families later, early gifts can grow in investment accounts, providing a head start when education costs arrive.

The levels and bases of taxation, and reliefs from taxation, can change at any time. The value of any tax relief depends on individual circumstances.

Further criteria applies within the HMRC IHT Manual IHTM04175 which is subject to change.

Around one-third of private-school pupils receive some level of fee assistance.³ Bursaries are based on financial need, while scholarships reward merit.

For professionals still building wealth, planning ahead by saving and investing now provides flexibility to supplement bursary awards or reduce the need for borrowing later.

3 ISC School Fee Assistance, April 2023

If you receive a large bonus or equity payout, some schools offer discounts for paying fees in advance. Compare the discount to potential investment returns before committing. Keeping some liquidity may offer greater flexibility as your goals evolve.

Should you require more information or have particular questions, we invite you to contact us at your convenience.

Contact Us

Nauman Gondal

Chief Executive Officer